Singapore Airlines: The Crown Jewel's Hidden Cracks

Is SIA still the premium investment it once was, or has competitive pressure turned Singapore's aviation pride into just another struggling airline?

Hey friends! Today we're diving deep into Singapore Airlines, a company that's close to every Singaporean's heart. Most of us see SIA as our national treasure, but the latest numbers tell a story that might surprise you.

I've been tracking SIA closely, and what I found will change how you think about this stock. Let's break down whether SIA deserves a spot in your portfolio or if it's time to look elsewhere.

The Revenue Story Looks Strong

SIA just posted record group revenue of S$19.54 billion for fiscal year 2025. That's a 2.8% jump from last year. The airline carried 39.4 million passengers, up 8.1% year-over-year. These are impressive numbers that show people still love flying with SIA.

Think of it this way: if SIA were a hawker stall, more customers are coming through the door than ever before. The passenger business alone brought in S$15.85 billion. That's serious money.

But here's where things get interesting. Revenue growth doesn't always mean profit growth.

The Profit Picture Tells a Different Story

While revenue hit records, operating profit crashed 37.3% to S$1.71 billion. That's like our hawker stall serving more customers but making less money per plate. Why? Competition is brutal.

Passenger yields dropped 5.5% as airlines flooded the market with cheap seats. When everyone's fighting for the same customers, prices fall. It's basic economics.

SIA's net profit of S$2.78 billion looks great on paper. But strip away the S$1.1 billion one-off gain from the Air India-Vistara merger, and the underlying business shows real pressure.

Cost Pressures Are Real

Total costs jumped 9.5% to S$17.83 billion while revenue only grew 2.8%. That's a recipe for margin compression. Non-fuel costs alone increased 11% to S$12.45 billion.

It's like running a business where your expenses grow faster than your income. Eventually, something has to give.

Fuel costs rose 6.1% to S$5.39 billion. With oil prices volatile, this remains a major risk factor for any airline investment.

Current Market Position

As of June 13, 2025, SIA trades at S$6.93, down 1.42% from the previous session. Analysts have a consensus target price of S$6.60, suggesting the stock might be slightly overvalued.

The overwhelming consensus? Hold, but don't expect fireworks.

The Dividend Bright Spot

SIA declared a total dividend of 40 cents per share for FY2025. That's 10 cents interim already paid in December 2024, plus a proposed 30 cents final dividend. The final dividend goes ex-dividend on August 8, 2025, and pays out on August 27, 2025.

For income-focused investors, this provides a current dividend yield of 5.8%. But remember, dividends depend on future profitability, which faces headwinds.

Strategic Positioning Remains Strong

The Air India partnership gives SIA a 25.1% stake in the enlarged Air India through the Vistara merger. This contributed the massive S$1.1 billion one-off gain to their bottom line. Think of it as buying a ticket to one of the world's fastest-growing economies.

SIA's operational metrics show disciplined capacity management. Singapore Airlines achieved a passenger load factor of 86.1% for the full year, while their budget subsidiary Scoot maintained 88.4%. The company expanded capacity by 8.2% while passenger traffic grew 6.4%.

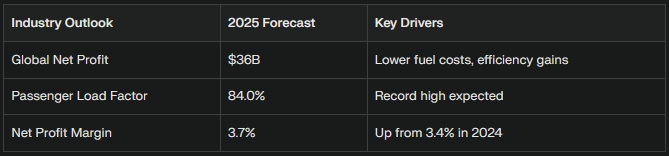

Industry Headwinds Ahead

The global aviation industry faces mixed signals. While IATA projects industry net profits to reach $36 billion in 2025, up from $32.4 billion in 2024, this comes with challenges. Revenue passenger kilometers are expected to grow 5.8%, but competition remains fierce.

For SIA specifically, analysts project FY2026 net profit to range from S$900 million to S$1.4 billion - a significant drop from the current S$2.78 billion when you strip out the one-off gain.

My Investment Take

SIA remains a quality company with strong fundamentals. The brand, operational efficiency, and strategic positioning are real competitive advantages. But industry dynamics are working against profitability.

My rating: Cautious Hold with accumulation on significant dips.

For dividend investors, SIA offers decent income with a current yield of 5.8%. But don't expect significant growth in payouts given the margin pressure.

For growth investors, wait for a better entry point. If the stock drops below S$6.00, it might present value.

Practical Action Items

Portfolio Allocation: Keep SIA under 5% of your total portfolio if you own it

Entry Strategy: Consider dollar-cost averaging if you're bullish long-term

Exit Triggers: Watch for operating margins below 8% as a warning sign

Dividend Dates: Mark August 8, 2025 (ex-dividend) and August 27, 2025 (payment) in your calendar

The Bottom Line

SIA isn't broken, but it's not the growth story it once was. The aviation industry is mature, competitive, and cyclical. While SIA remains the premium player, premium doesn't always mean premium returns.

Think of SIA as a bond with some upside potential rather than a growth stock. It's suitable for conservative portfolios seeking steady income, but probably not the best choice for aggressive growth strategies.

The key is managing expectations. SIA will likely remain profitable and pay dividends, but explosive growth seems unlikely given current industry dynamics. The 37.3% drop in operating profit despite record revenue tells the real story - this is a company fighting margin compression in an increasingly competitive market.